Debt Ceiling Jeopardizes Dollar’s Reserve Status

Axel Merk, Portfolio Manager, Merk Funds May 24, 2011

U.S. Treasury Secretary Geithner has warned that delays in extending the U.S. debt ceiling may cause irreparable harm. While borrowing costs for the U.S. government have not yet risen, irreparable harm may have already been done to the U.S. dollar and its status as a reserve currency. Ironically, it’s not a plunging, but a rallying bond market that is a symptom of the problem. Let us explain.

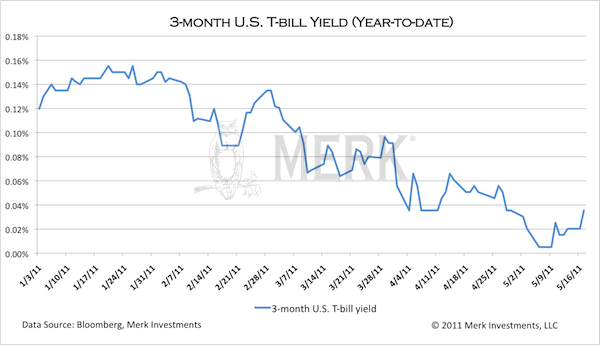

First, no one really knows how the markets will behave should the U.S. delay servicing its debt. Most observers believe that a) the Treasury has a big bag of tricks to continue servicing the debt; and b) politicians will play a game of chicken, but eventually do what they always do: agree to spend more money. Some have even suggested that a derailment of the bond market may not be the worst outcome, as it forces action on the deficit now rather than later, arguing that in the long-run, this would be a positive development. That said, we don’t know how the bond market will react; but we do know that policy makers are playing with fire, and when you play with fire, you may get burned. For the time being, there is a more imminent problem building in the markets that may have long-lasting effects. At this stage, the U.S. government may roll existing debt, but cannot issue new debt. This has created a situation where fear may be spreading that there simply won’t be a large enough supply of debt to meet investor demand. While this sounds like an odd problem to have, we have recently witnessed a rather unusual level of investment flows, with money piling into Treasuries. As of this writing, investors receive a paltry 0.04% annualized return on their money for giving Uncle Sam a 3-month loan. That’s a third of the yield available at the beginning of the year, when 3 month U.S. Treasury Bills yielded an annualized 0.12% (already a severely depressed yield):

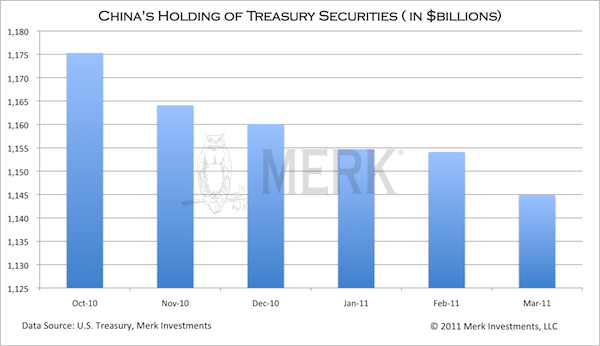

For the time being, this is mostly an oddity. But this may well have profound long-term implications for investors from domestic institutions to foreign central banks. Our main concern, however, is with foreign central banks. A key reason why the U.S. dollar has been the world’s reserve currency is because of the lack of alternatives. And when we talk about a lack of alternatives, we don’t talk quality, but liquidity. When you have billions to deploy, but don’t want to rock the markets, the U.S. Treasury markets have historically been the most liquid in the world. The People’s Bank of China, for example, has been increasing its gold holdings; however, as a percentage of its reserves, gold holdings have been going down as total reserves have been climbing at an even faster pace. Liquidity concerns may be the main driver behind this, as the gold market is far less liquid than the Treasury markets. Like most central banks, the People’s Bank of China typically does not try to influence market prices, thus adjusting any involvement based on liquidity considerations. It’s not just the gold market, though. As far as money markets are concerned, the U.S. has the deepest, most liquid market in the world. Indeed, one of the best ways to increase global stability would be for Asian countries to develop their domestic fixed income markets, so that Asian issues of debt are less dependent on the U.S. dollar. But even the Eurozone with an active market in German and French Treasuries, to name a few, is a distant second to the U.S. Our concern is that the building scarcity of Treasuries will force central banks elsewhere to deploy their money outside of the U.S. Treasury market. As foreign central banks gain operational experience in less liquid markets, they may not revert back to U.S. Treasuries once the gridlock on Congress is resolved. Note that central banks often buy longer dated securities, but we use 3 month bills to illustrate the issue, as those bills should not change all that much in value absent of a change in Federal Reserve policy. Of course, if the scarcity of Treasuries were a result of less deficit spending in the U.S., it would be an entirely different story. But given that the U.S. depends on a vivid Treasury market for a seemingly ever-escalating deficit, the implications of alienating large foreign investors could be dire. In that context, it is worth noting that China has been reducing its Treasury holdings rather steadily:

We are not predicting that institutional investors will abandon the Treasury markets in the near future, but the damage created by a failure to raise the debt limit can already be seen in the markets. As investors, domestic and foreign, learn to deal with reduced liquidity in the Treasury markets, they will have to deploy money elsewhere. As such, foreign central banks may accelerate their diversification beyond the U.S. dollar as operational experience is gained and liquidity may increase in other markets. In the short-term, another driver may be that the artificial shortage of Treasuries make their yields unattractively low, thus encouraging rational investors to look elsewhere for less manipulated returns.

Please join us for a Bloomberg Webinar on May 26 where we will discuss the other side of the coin: the future of the euro in the context of U.S. and Eurozone challenges (click here to register). To be updated as this discussion evolves, please make sure you sign up to our newsletter. We manage the Merk Absolute Return Currency Fund, the Merk Asian Currency Fund, and the Merk Hard Currency Fund; transparent no-load currency mutual funds that do not typically employ leverage. To learn more about the Funds, please visit www.merkfunds.com. Manager of the Merk Hard, Asian and Absolute Currency Funds, www.merkfunds.com Axel Merk, President & CIO of Merk Investments, LLC, is an expert on hard money, macro trends and international investing. He is considered an authority on currencies. The Merk Hard Currency Fund (MERKX) seeks to profit from a rise in hard currencies versus the U.S. dollar. Hard currencies are currencies backed by sound monetary policy; sound monetary policy focuses on price stability. The Merk Asian Currency Fund (MEAFX) seeks to profit from a rise in Asian currencies versus the U.S. dollar. The Fund typically invests in a basket of Asian currencies that may include, but are not limited to, the currencies of China, Hong Kong, Japan, India, Indonesia, Malaysia, the Philippines, Singapore, South Korea, Taiwan and Thailand. The Merk Absolute Return Currency Fund (MABFX) seeks to generate positive absolute returns by investing in currencies. The Fund is a pure-play on currencies, aiming to profit regardless of the direction of the U.S. dollar or traditional asset classes. The Funds may be appropriate for you if you are pursuing a long-term goal with a currency component to your portfolio; are willing to tolerate the risks associated with investments in foreign currencies; or are looking for a way to potentially mitigate downside risk in or profit from a secular bear market. For more information on the Funds and to download a prospectus, please visit www.merkfunds.com. Investors should consider the investment objectives, risks and charges and expenses of the Merk Funds carefully before investing. This and other information is in the prospectus, a copy of which may be obtained by visiting the Funds' website at www.merkfunds.com or calling 866-MERK FUND. Please read the prospectus carefully before you invest. The Funds primarily invest in foreign currencies and as such, changes in currency exchange rates will affect the value of what the Funds own and the price of the Funds' shares. Investing in foreign instruments bears a greater risk than investing in domestic instruments for reasons such as volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, and relatively illiquid markets. The Funds are subject to interest rate risk which is the risk that debt securities in the Funds' portfolio will decline in value because of increases in market interest rates. The Funds may also invest in derivative securities which can be volatile and involve various types and degrees of risk. As a non-diversified fund, the Merk Hard Currency Fund will be subject to more investment risk and potential for volatility than a diversified fund because its portfolio may, at times, focus on a limited number of issuers. For a more complete discussion of these and other Fund risks please refer to the Funds' prospectuses. This report was prepared by Merk Investments LLC, and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice. Foreside Fund Services, LLC, distributor.

Thank you for your interest in the Merk perspective. To serve our audience better and to continue offering our insights free of charge, please enter your information below to continue reading.

|

||||||||||||||||||